Name of QuantLet: IDA_localising

Published in: Institute for Digital Assets (IDA)

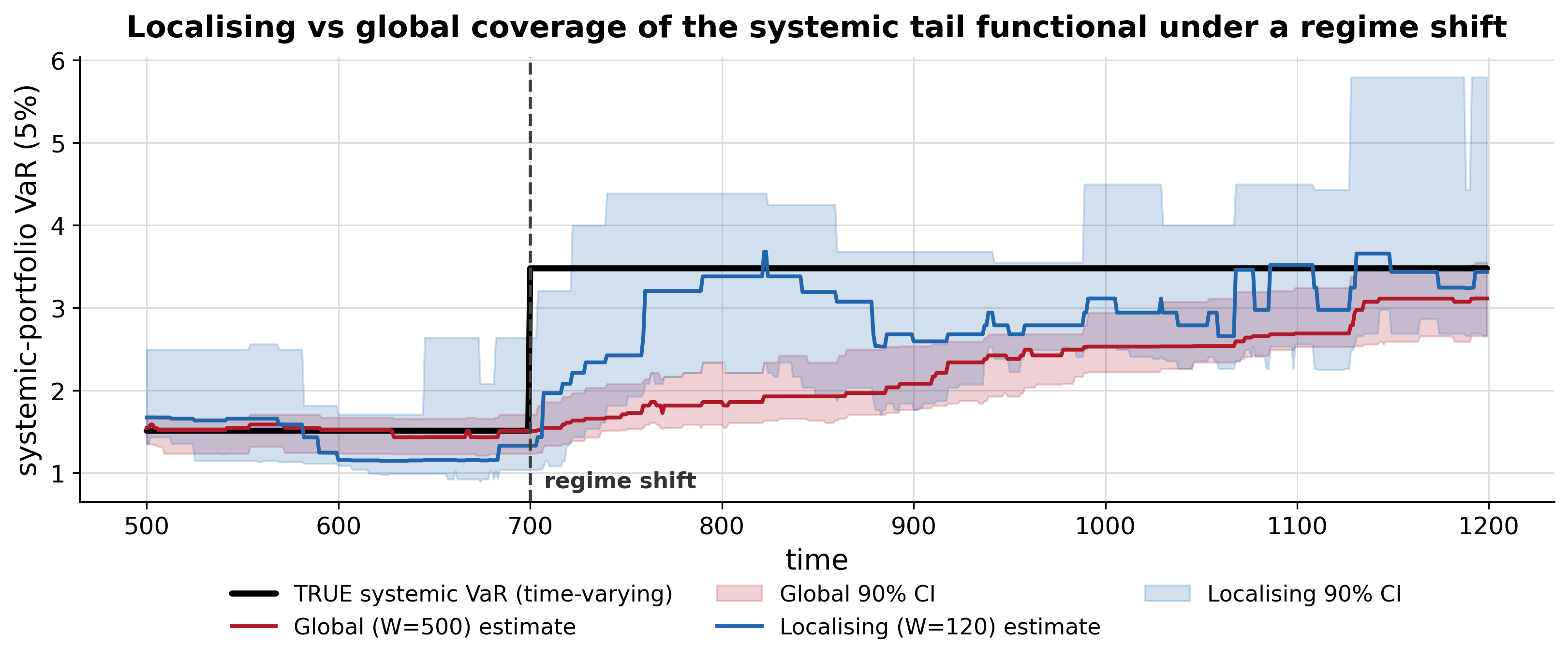

Description: Controlled Monte-Carlo diagnostic (300 paths) showing that a localising (adaptive-window, Haerdle ICARE / Localizing-CAViaR style) estimator restores reliable coverage of a time-varying systemic tail functional under a regime shift, where a global stationary estimator does not. The functional is the 5% Value-at-Risk of the principal-eigenvector (systemic) portfolio of a 12-asset network; distribution-free order-statistic 90% confidence intervals are used. Under a volatility regime shift at t=700 the global estimator''s coverage collapses (about 92% to 33%) while the localising estimator holds near nominal (about 94% to 89%) and roughly halves RMSE - evidence for the L2 reliability mechanism (not the full high-dimensional theorem).

Keywords: value-at-risk, systemic risk, tail risk, localising estimation, adaptive window, non-stationarity, regime shift, coverage, confidence interval, Monte-Carlo, CAViaR, ICARE

Author: Daniel Traian Pele

Submitted: 25 June 2026

Output: o1_localising.png, o1_results.md

Example: o1_localising.png - true time-varying systemic VaR with global vs localising estimates and their 90% confidence bands; after the regime shift the global band loses coverage while the localising band retains it.

{kind=link}